3D Secure Payment

Protect online card payments with the 3D Secure system - without rebuilding your checkout.

Let’s Talk

What is 3D Secure with Fenige?

3D Secure payment system is an authentication protocol that adds an additional security step to card-not-present transactions. The system asks the cardholder to verify their identity (for example, with a one-time code, mobile app, or biometric check) before the payment is finalized.

Fenige uses 3D Secure:

E-commerce Acquiring for Consumers’ Payments with 3D Online Payments

Money Transfer funding transactions with additional protection for 3DS transactions

Where it fits in your stack

3D Secure is relevant if you:

Accept Online Card Payments

through Fenige’s E-commerce Acquiring solution or PaymentHub

Operate a Platform or Marketplace

as Payment Facilitator and need secure payment flows

Originate Money Transfer transactions

where issuers or regulations require strong authentication

Must Comply with PSD2 SCA or Similar Regulations

operate in regions where PSD2 Strong Customer Authentication (SCA) and similar rules expect 3DS for online payments.

You keep your existing checkout and business logic; Fenige provides the 3DS rails and handles the protocol details with Visa Secure, Mastercard Identity Check and other scheme programs that are based on the 3D Secure standard.

Key benefits

Stronger security for online payments

The 3D Secure system adds an extra verification step on top of payment credentials. This significantly increases transaction security and helps prevent unauthorized transactions.

Helps you meet SCA requirements

In Europe and other regulated markets, SCA under PSD2 requires two-factor authentication for card-not-present transactions. 3D Secure payment flows are the standard way to meet these regulations and reduce compliance risk.

Better customer trust

Educational content on

fenige.com explicitly recommends 3D Secure as a key protection for safe online payments. Using it shows customers that you take security seriously, which supports higher trust and repeat purchases.

Modern 3DS 2.x experience

Fenige powers dynamic 3D Secure 2.x, which supports a frictionless flow for low-risk payments. Compared to the old 3DS 1.x, this makes the experience smoother and more mobile-friendly while still adding security.

No need to run your own 3DS server

Fenige’s E-commerce Acquiring & 3D Secure suite is a complete solution based on Fenige’s API - there’s no need to build your own processing or get separate scheme certifications for 3DS.

How 3D Secure Payments Work with Fenige

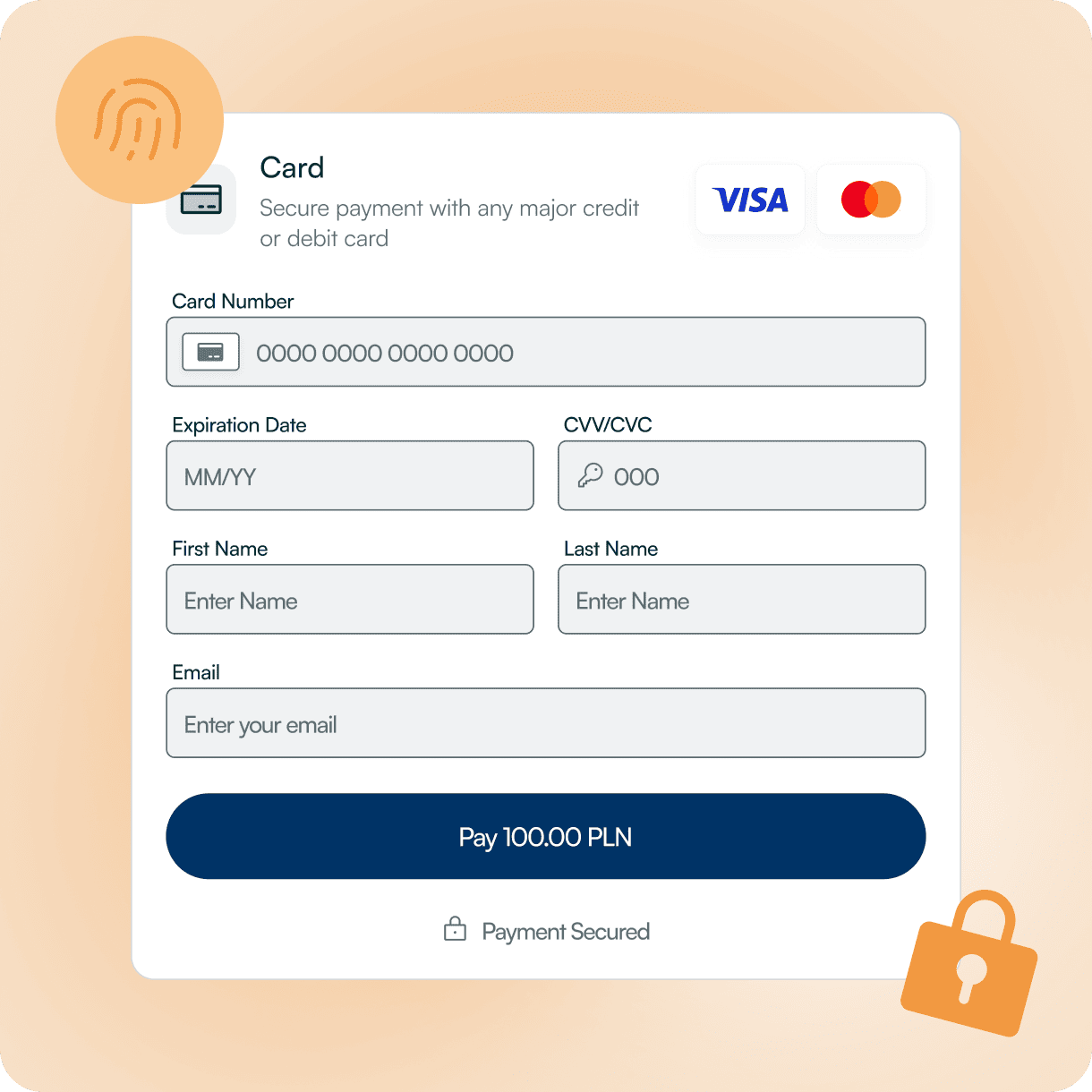

Customer starts a payment

The customer enters card details or pays with a tokenized card / wallet (for example, Google Pay via PaymentHub).

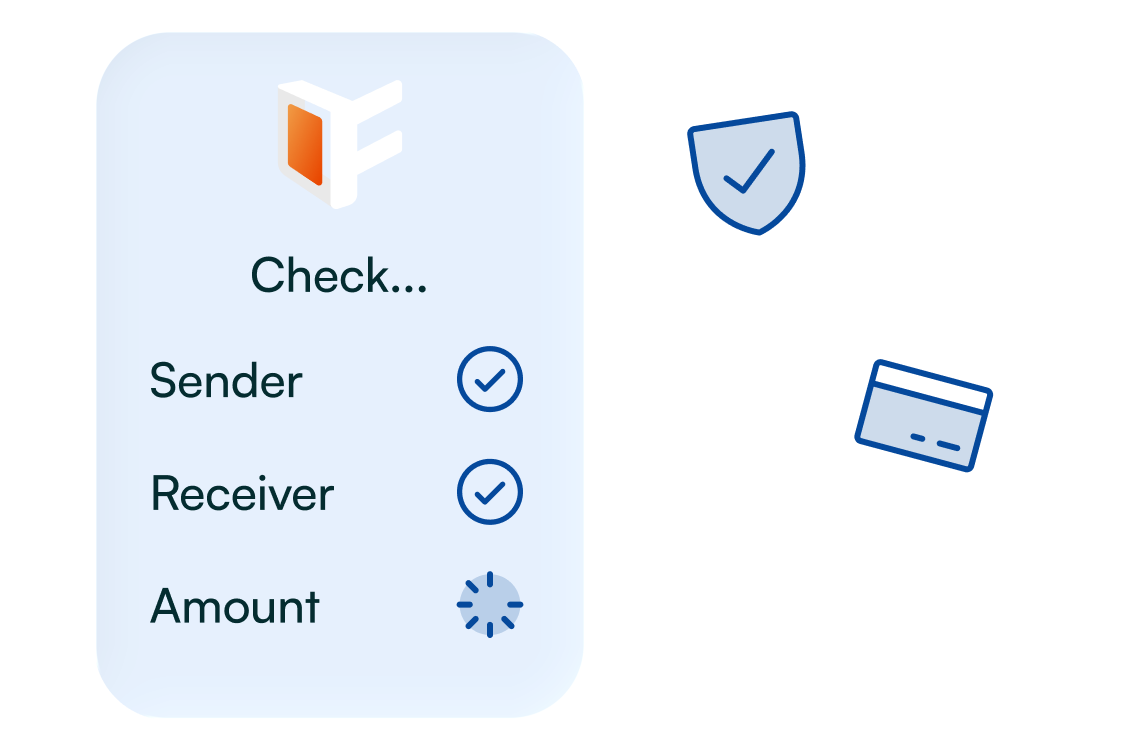

Fenige checks if authentication is needed

Based on card-scheme rules, issuer requirements and regulatory context, Fenige determines whether the transaction requires a 3D Secure authentication step.

Issuer authenticates the cardholder

If authentication is required, the system prompts the customer to confirm the payment (for example, with an SMS code, bank app push, or biometric check). The verification requests propagates from the acquirer, through the card-scheme, and reaches the issuer who completes the validation process. Only a positive result of the 3-D Secure Procedure allows the transaction to proceed.

Fenige completes or declines the transaction

Fenige receives the 3DS result from the issuer and either completes the authorization or rejects the transaction if authentication fails.

FAQ

3D Secure is an authentication system that adds an extra verification step to online card payments, helping confirm the cardholder’s identity before a payment is completed.

How does 3D Secure protect online payments?

The 3D Secure system reduces fraud by requiring additional authentication during a 3D Secure payment, such as a one-time code, banking app approval, or biometric verification.

Is 3D Secure required for PSD2 SCA compliance?

In many regions, PSD2 Strong Customer Authentication (SCA) requires 3D Secure online authentication for card-not-present transactions to meet regulatory standards.

Does 3D Secure affect the checkout experience?

Modern 3D Secure 2.x enables a frictionless flow for low-risk transactions, allowing many payments to be completed without user interruption while still applying strong security when needed.

Can 3D Secure be integrated without changing checkout logic?

Yes, Fenige provides the 3D Secure system as part of its acquiring infrastructure, allowing businesses to keep their existing checkout while Fenige handles authentication and protocol details.

Want to secure your online card payments with 3D Secure and stay compliant?

Let’s Talk